When constructing an investment portfolio, one of the fundamental allocation decisions is between public and private markets. Most institutional portfolios hold both, but understanding the key differences is essential for developing a strategy aligned with your financial objectives, time horizon, and allocation constraints.

At a high level, the tradeoff is straightforward. Public markets offer high liquidity, price transparency, low investment minimums, more regulatory oversight, and lower fees. However, they are also characterized by short-term volatility, sentiment-driven “herd” behavior, and exposure to broader market swings. Most importantly, in today’s information rich environment, much of the upside is often already priced-in, making it very difficult to develop an edge and generate alpha. In fact, most professional investors rarely outperform market indices over prolonged periods of time.

On the other hand, private markets offer access to assets and strategies beyond public exchanges, with lower correlation to broader markets and a history of outperformance at the top end. However, they require longer holding periods, remain inaccessible to most investors, are inherently illiquid, and typically come with higher costs.

Therefore, the debate is often framed as liquidity and accessibility versus return potential and exclusivity. In most industries, this framework is sufficient. In shipping, it is not.

The case of Shipping

Shipping is undoubtedly underrepresented in stock exchanges. While it facilitates most of the global trade, only a small fraction of the industry is accessible through public equities.

Maritime transport moves up to 90% of global goods, yet less than 5% of the global fleet is owned by publicly listed companies – and once free float and trading liquidity are taken into account, the investable universe is materially smaller.

The vast majority operates in private hands — family offices, private equity funds, and independent shipowners. This is NULL, not a coincidence. It reflects a deeper incompatibility between the way shipping generates returns and the way public markets price risk.

Public Markets: Indirect Exposure

Public shipping equities provide an accessible entry point to the industry, albeit limited and not in a pure form. When investors purchase shares in a listed shipping company, they are not acquiring a direct stake in vessels. Instead, they are buying into a corporate structure layered with additional variables:

- Fleet composition

- Operational strategy

- Capital structure

- Management decisions

- Investor perception

- Broader equity market sentiment

This weakens the link to asset-level performance, reducing shipping fundamentals to just one component of the broader investment thesis. The implication is clear: investors approaching shipping through public markets are often engaging with a filtered, and potentially distorted, version of the asset class.

Shipping is an asset-driven industry with characteristics closer to real estate, infrastructure, or aviation leasing, rather than to traditional corporate equities. Vessels are long-lived, capital-intensive assets, typically operating over a 20–25 year economic life, whose value is tied to prevailing market conditions, replacement costs, and supply-demand dynamics.

Value creation follows a simple formula: cash flows are generated by charter income, while asset repricing across cycles amplifies investment outcomes. In contrast, public equity frameworks generally rely on discounted cash flows or earnings multiples to value a firm based on its long-term operational growth and perpetual income streams. This disconnect creates a persistent structural anomaly: the discount to Net Asset Value (NAV).

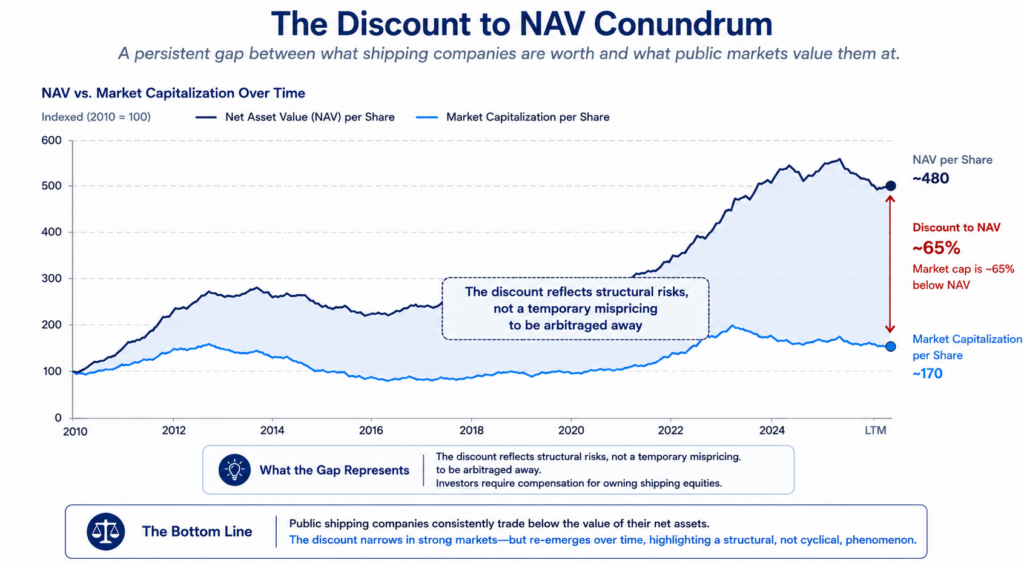

The discount to NAV conundrum

A defining feature of public shipping equities is their tendency to trade at a discount to net asset value (NAV). In theory, this should present an opportunity. If a company’s fleet (net of debt) is worth more than its market capitalization, investors appear to be acquiring assets at a discount. Historically, this argument has been used to justify investments in listed shipping companies. However, empirical evidence suggests that the discount rarely closes in a sustained manner. While valuations may temporarily converge during strong markets, the discount tends to re-emerge over time. This persistence suggests that it is not a transient inefficiency, but a structural reality.

Public markets are applying a discount to account for the risks embedded in the corporate structure. The result is a stable equilibrium in which shipping companies are consistently valued below the sum of their parts, suggesting that the NAV discount is not a mispricing to be arbitraged away.

Private Markets: Alignment with Fundamentals

Private investment structures offer a markedly different approach while unlocking a far larger opportunity set. Through direct or near-direct ownership of individual vessels or defined portfolios, investors:

- Align more closely with the fundamental drivers of value

- Gain a high degree of selectivity, enabling them to effectively cherry-pick individual assets

- Can achieve meaningful diversification by allocating capital across multiple operators and strategies

- Enjoy returns insulated from public market noise and grounded to asset-level economics

- Maintain greater influence over strategic decisions

Further, unlike public equities, private investments are not continuously marked to market, reducing observed volatility and shifting the focus away from short-term fluctuations to what matters most: asset selection, entry discipline, exit timing, and the patience to navigate the cycle.

Reframing the Core Tradeoff

In traditional portfolio theory, capital allocation between public and private markets is framed around liquidity and accessibility versus return potential and exclusivity. In shipping, this tradeoff evolves into something more fundamental:

| Public | Private | |

| Opportunities set | Limited set of listed companies | Broad access to majority of the industry |

| Exposure | Indirect, via corporate structures | Direct, at the asset files-level |

| Return drivers | Market sentiment, investor perception, governance | Charter income and asset value delta |

| Valuation | Driven by equity market frameworks and market sentiment | Anchored in asset-level fundamentals |

| Liquidity | Higher, though often overstated | Lower, but supported by an active secondhand vessel market |

| Control | Limited | Greater influence |

| Transparency | High, but backward-looking, with disclosures often lagging real-time market conditions | Lower, but more asset specific |

Public markets provide liquidity, but at the cost of structural complexity and persistent valuation discounts. Private markets require patience and acceptance of illiquidity, but offer a more direct path to capturing the underlying economics of the industry.

This helps explain why institutional capital has long favored private structures in shipping. The industry rewards timing, discipline, and asset selection—characteristics that are more easily expressed in private investment frameworks.

Expanding Access

Limited access has historically been the defining constraint of private markets, and shipping is no exception. Participation requires industry relationships, significant capital commitments, and specialized expertise, therefore restricting the opportunity set to a select few.

This is beginning to change. Across asset classes, a broader structural shift is underway, with capital increasingly allocated to private markets in search of diversification, differentiated return profiles, and exposure to real assets. At the same time, a global push toward financial inclusion is expanding access to investment opportunities that were previously out of reach. Shipping sits at the intersection of these dynamics. As a predominantly private, asset-driven industry, it has historically remained inaccessible to most investors despite its central role in global trade.

Technology, digital platforms, and regulatory evolution are bridging that gap. Solutions such as Helm are designed to provide investors with the tools to access institutional-style shipping opportunities, while lowering barriers to entry and improving transparency, empowering a broader investor base to engage directly with the asset-level economics of the industry.

Closing Perspective

The traditional framework for allocating between public and private markets remains a useful starting point. Liquidity and accessibility on the one side; exclusivity and return potential on the other. In shipping, however, the distinction runs deeper.

Public markets offer access to the industry, but often through a lens that dilutes and distorts the underlying economics. Private markets, while less accessible, provide a much wider opportunity set, and closer connection to the assets and value drivers that define shipping as an asset class.

The persistent discount to NAV of public shipping equities is the clearest signal of this divergence. It reflects not a temporary inefficiency, but a structural difference in how markets value assets versus the entities that own them.

The choice is not between public and private. It is between exposure to shipping as a corporate construct, and exposure to shipping as a real asset.