Who are the shipping industry participants?

Shipping quietly moves the world. Roughly nine-tenths of international trade by volume travels by sea, making maritime transport one of the most essential, albeit least visible, industries in the global economy.

Yet behind every cargo movement sits a sophisticated ecosystem of overlapping constituencies, each with its own economics, incentives, and sources of power. The industry is built on a layered architecture in which ownership, operation, financing, insurance, and regulation are divided among different actors, supported by a wide network of specialist service providers. So to understand shipping, one must first break down its true cast of participants.

Shipowners: the asset holders

Everything begins with the shipowner. Shipowners own the vessel as a capital asset and decide how it will be employed, financed, maintained, and eventually sold or recycled. In market terms, they provide supply. In practical terms, shipowners are the industry’s landlords: they own scarce transport capacity and lease it to the market.

Owners range from century-old family enterprises to listed corporations, sovereign-backed fleets, private equity vehicles, leasing houses and industrial conglomerates. Their role is to deploy capital into ships and, while doing so, absorb market cyclicality through freight exposure, asset values, residual risk, regulation and financing costs. In buoyant markets they benefit from both strong operating cash flows and rising asset values; in weak markets they are called to demonstrate discipline, navigate the rough seas of fixed vessel operating expenses, financing costs, and absorb market cyclicality.

That delicate balance is precisely what has given rise to highly specialized shipowning cultures in places such as Greece, Norway, Japan and China, where maritime know-how has been refined across generations and is practiced as much as craft as a business. The rewards for getting it right can be extraordinary. Few industries combine operating leverage and asset-price upside in a way that can generate such outsized returns. At its peak, that has allowed the most capable shipowners not merely to compound capital, but to create outsized fortunes and enduring generational wealth.

Charterers: the demand side of the market

If shipowners supply transport capacity, charterers create demand for it. A charterer is the party that hires the ship, whether for a single voyage, a period of time, or a longer contractual program. Charterers are often commodity producers, oil majors, traders, mining companies, utilities, steel mills, grain houses, container lines, and even governments.

Examples include blue-chip multinationals such as Shell, BP, ExxonMobil, Cargill, Glencore, BHP, Rio Tinto, Maersk, MSC, CMA CGM.

Charterers occupy a position of exceptional importance because they determine how cargo demand is expressed in the freight market — by geographical trade route, timing, volume and contractual structure. They are not merely customers purchasing transport, but strategic counterparties whose commercial approach and contracting behavior can materially alter market direction and, at times, reshape entire segments.

Operators: the commercial intelligence layer

Between the shipowner and the charterers often sits the operator. Operators may not own ships at all; instead, they charter vessels from owners and redeploy them into the market, matching cargoes, managing scheduling, arbitraging geography, and extracting margin from information, timing and execution. It is where market intelligence and information asymmetry is monetized.

This matters because shipping is not governed by abstract equilibrium alone. Small advantages in timing, information and execution can translate into meaningful commercial outcomes. The best operators do not simply fix ships; they optimize deployment, anticipate dislocation and turn market complexity into margin.

Ship managers: running the vessel day-to-day

A ship is a capital asset, but also a floating industrial plant requiring constant technical and operational management. Someone must crew it, maintain it, provision it, insure it, document it, and keep it in compliance with regulatory requirements. That function belongs to ship managers, whether in-house within an owner’s organization or outsourced to third-party specialists.

Their importance is often underestimated by non-maritime observers. Yet poor ship management can quickly erase commercial profits. While owners, charterers, financiers, and brokers negotiate deals in boardrooms, the ships themselves never stop working, and neither do the people who run them.

Brokers: the market makers

Shipping remains, in many respects, one of the last major relationship-driven markets. Brokers serve as the connective tissue, linking participants in several distinct ways: chartering brokers align cargo demand with vessel availability, sale-and-purchase brokers match ship buyers with sellers, and finance brokers connect owners with the capital needed to acquire, renew or expand fleets.

If that sounds modest; it is not. Brokers are information nodes. They help establish price discovery and are often the first to sense a tightening basin, a distressed seller, a financing squeeze or a shift in cargo demand. Proximity to information is power and this is why brokers monetize access, relationships and market intelligence.

Financiers: the enablers of fleet growth

Shipping is capital-intensive and structurally dependent on reliable access to patient, well-timed capital. A modern vessel can cost tens or even hundreds of millions of dollars and historically, most shipping investments that have gone wrong were not because of asset selection, but because the capital behind them was poorly structured, mistimed or too expensive.

The current ship financing landscape includes banks, leasing houses, export credit agencies, bond investors, private credit funds, private equity, public equity and specialist alternative managers.

Shipyards: the manufacturers of future supply

A shipyard is the industrial facility where ships are designed, assembled and constructed. It is where raw steel, engineering systems and specialized marine equipment are turned into working commercial vessels. They do not own ships, carry cargo, or earn freight, but affect how much future transportation capacity will exist, how quickly it can be delivered, at what cost, and with what technology embedded in it.

Their importance extends well beyond construction. Every new vessel must be ordered, priced, scheduled and built years before it can compete for cargo. That makes shipyard capacity one of the most critical constraints in shipping economics and can affect the market before a vessel ever hits the water.

This part of the industry is also one of the most geographically concentrated parts of the maritime economy. Modern commercial shipbuilding is dominated by China, South Korea and Japan — the three strongest shipbuilding nations in the world. China leads in scale and order volume, South Korea remains especially strong in high-specification tonnage, and Japan continues to lead in build quality and tradition.

Insurers: the risk transfer specialists

Marine insurance is not ancillary to shipping. It is structural. The two dominant insurance pillars are “Hull and machinery” protecting against physical vessel damage and “protection and indemnity clubs” addressing third-party liabilities, from collision and cargo claims to pollution and crew matters.

That coverage does more than cushion losses. It underwrites market confidence. Without insurance, financing is impaired, port access becomes difficult, trading patterns narrow, and counterparty risk widens. In other words, insurance is what makes global shipping tradable.

Classification societies: the technical gatekeepers

Classification societies are neither owners nor regulators, yet they are indispensable to both. Classification societies are independent technical organizations that set design, construction and maintenance standards for ships, surveys them throughout their lives, and issues the class certification that confirms the vessel meets those standards.

In commercial terms, class is a passport. A ship that is not maintained in class can quickly become difficult to insure, harder to finance, less attractive to charterers and, in some cases, unable to trade at all. Class therefore acts as a form of technical credibility: it signals that the vessel has been built, maintained and surveyed to an accepted standard.

The leading classification societies — including DNV, Lloyd’s Register, ABS, Bureau Veritas, ClassNK and RINA — are part of the framework that keeps a ship economically credible throughout its operating life.

Flag states, IMO and regulators: the sovereign layer

Flag states are the jurisdictions under whose laws ships are registered and entitled to sail. They play a central role in shaping the legal and regulatory framework within which a vessel operates, influencing compliance obligations, inspection standards, crewing rules and, in some cases, how counterparties perceive the ship’s overall quality and governance.

Yet flag states do not operate in isolation. They sit within a much broader international regulatory system, anchored by the International Maritime Organization (IMO), the United Nations agency responsible for the global rulebook of shipping. The IMO develops the standards that govern how ships are designed, equipped, operated and monitored, with its mandate centered on safety, security, environmental protection and the facilitation of international maritime traffic.

From there, the wider regulatory architecture extends outward: flag states enforce these rules on ships under their jurisdiction, port states inspect vessels calling at their ports, classification societies verify technical compliance, while national and regional authorities shape areas such as sanctions, competition, taxation, labor standards and environmental performance. Collectively, these institutions shape the legal, technical and commercial framework of the industry.

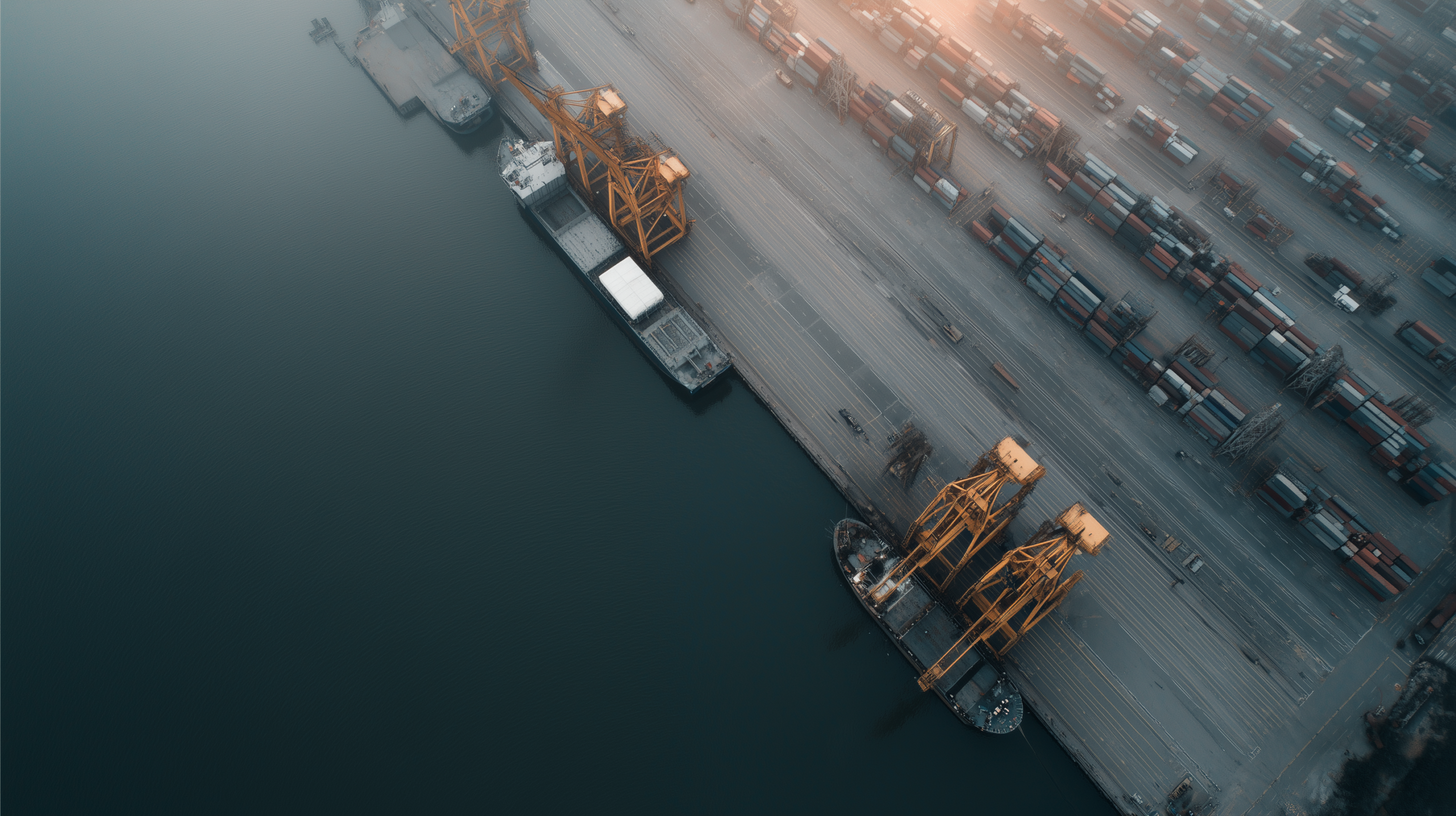

Ports and terminals: the physical nodes of the ecosystem

Ships are only productive when they can load and discharge cargoes efficiently. Ports, terminals, pilots, towage providers, bunkering services, customs agencies and clearance systems are the physical and administrative nodes through which maritime transport becomes real. In a world of disruptions, sanctions, congestion and rerouting, ports are active determinants of effective vessel supply.

Seafarers: the labor force without which nothing moves

Every discussion of shipping participants eventually arrives at the same reality: ships do not trade themselves. Seafarers remain the indispensable operating workforce of the industry, responsible for navigation, engineering, cargo operations, maintenance and onboard safety.

Their importance is self-evident, albeit often overlooked. That is a mistake. Shipping is asset-heavy, but it remains irreducibly human.